“To a herd of rams, the ram the herdsman drives each evening into a special enclosure to feed and that becomes twice as fat as the others must seem to be a genius. And it must appear an astonishing conjunction of genius with a whole series of extraordinary chances that this ram, who instead of getting into the general fold every evening goes into a special enclosure where there are oats- that this very ram, swelling with fat, is killed for meat”. – Tolstoy, ‘War and Peace’.

After so many false dawns, the recent announcement by Spain’s Prime Minister Mariano Rajoy that the government was revising down its 2013 economic forecast hardly caused a blink among a citizenry that is now completely inured to deception and ready to believe the worst about the intentions of any politician willing to come forward with either good or bad news. The long announced recovery has once more been delayed, and will now be noted not in the last three months of this year, but during the first six of 2014. Naturally, a public which is now totally accustomed to such postponements will not be surprised if this one is far from being the last.

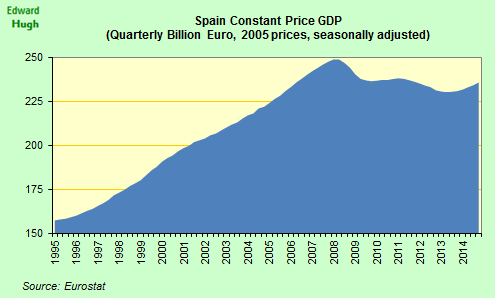

In fact, the latest institution to throw a bucket of cold water over the Spanish government’s rose-tinted promises is the IMF. In their latest five-year forecast for Spain they paint a pretty bleak picture of low growth and high unemployment lasting at least all through what is left of the present decade. Mariano Rajoy has already jumped into the fray to take issue with their outlook for 2013, but it is their longer-term forecast which is most interesting and preoccupying. Growth between 2015 and 2018 is now only expected to average around 1.5 percent annually. This would seem to be what the IMF now consider longer-term trend growth to be for Spain, and the most notable thing about the number is that it represents a significant downward revision from their earlier optimism. Even this comparatively low number may still be overly optimistic and may yet come down again – I personally expect NO noticeable recovery as cumulative negative developments more or less cancel out positive ones – but it is certainly much more realistic than anything we have seen from the Fund before. There is no question here of any “V” shaped bounce. That is just a fiction of Finance Minister Cristóbal Montoro’s imagination.

Naturally, the other side of the coin on this is the consequence for unemployment. With growth so low there will be little in the way of job creation (watch out, pension system sustainability) and unemployment will linger over 20 percent for many years to come – indeed the IMF have 2018 unemployment at 22.9 percent, meaning they don’t expect it to fall below 20 percent come 2020.

And there’s another highly interesting detail from the IMF Spain forecast. Even to get that rather low level growth of 1.5 percent a year, the Fund pencil in Spain’s running a fiscal deficit of 5 percent a year all the way through to 2018, with the natural consequence that the debt-to-GDP ratio is expected to reach 110 percent by that point, and that isn’t making allowance for any further bank recapitalisation that will be needed. As I have been arguing since 2008 now, Spain’s sovereign debt simply is not on a sustainable path, and what 1.5-percent growth supported by a 5-percent fiscal deficit means is that there is no structurally adjusted growth going on in the economy at all. As a country you are getting more into debt than any increase in output you generate with the borrowing.

A well-oiled crisis

As I have argued in an earlier post, it may well be that the Spanish contraction machine is now so well-greased that it simply continues winding the economy down and down in such a way that things may never recover, in the classic sense of that term. The only argument which stands in the way of reaching this conclusion is the near religious belief now so often heard in policy circles that, well, “economies always recover, don’t they?”

As it happens, they don’t, as a quick look at what happened in Argentina in the 20th century would confirm. But Argentina is arguably an isolated case, and the current economic malaise (I hesitate to use the word “crisis” due to the duration of what is so evidently an ongoing process) seems to be far more general. What people seem to find hard is asking themselves one simple question, “but what if this time really is different?” Which is strange, since reasons for thinking that things may well not return to what was previously considered “normal” are not in short supply.

Populations in developed economies are all now ageing rapidly, generating a phenomenon never before seen in the entire history of known human societies – systematically falling numbers of under-15s coupled with an ever growing population in the over-80s group. The sheer novelty of this phenomenon, coupled with the manifest feeling of unsustainability it generates about our current welfare arrangements should at least give policy makers food for thought, yet evidence that it actually is doing so is in very short supply. Plough on regardless seems to be the watchword.

The current round of cuts to health and education spending are described as “painful but necessary” in order to facilitate a return to growth which will make further adjustments in the future unnecessary. Unfortunately nothing could be farther from the truth. The credit ratings agency Standard & Poor’s, which has been one of the global leaders in highlighting the likely impact of “first world” demographic changes, argues in its latest report on the subject that despite some recent progress, without ongoing and continuous changes in provision entitlement, deficits and debt in developed economies will spiral out of control as the century advances.

I think everyone who stops and thinks for five minutes about the situation will recognize the obviousness of this point, yet scarcely a single politician is willing to come out from behind the curtain and explain to voters the longer-term implications of having shrinking and ageing workforces at the same time as the size of retirement age populations explodes.

Ignoring the obvious

By the middle of this century, and without policy changes, average deficits for developed countries will rise to 15.1 percent of GDP as the interest cost of the increasing debt burden exacerbates the budgetary impact of demographic spending. Median general government NET (not gross) debt (as a percentage of GDP) is expected to increase to 71 percent by the mid-2020s (from around 40 percent today) – and would then accelerate to 216 percent of GDP by 2050. Government spending would rise to about 57 percent of GDP in 2050, from some 49 percent today.

Naturally, these numbers are just very rough and ready estimates, and such levels are unlikely to be reached since markets will surely not fund them, and policy changes will happen. The problem is that many policy makers are still stuck in denial about the need to make them, and where they are willing to do so it is largely linen washing conducted in private and not in the public space provided by election manifestos. Spain’s leaders, for example, continue to insist that no major changes in either pension contributions or entitlement are in the offing even though the need for one or the other is evident, as the structural deficit in the system continues to grow.

Worse, the more frequently they say in public that there is nothing to worry about and all is well, the lower their credibility falls, since few people continue to believe them. At the same time they insist and insist that the current level of health provision will be maintained no matter what, when obviously this is something the country simply cannot afford to do.

But more than the simple impact on government spending possibilities, it is the impact of these demographic changes on growth which seems to be the least widely appreciated part of the story. This is not an oversight of which Standard and Poor’s is guilty. According to the agency:

For several sovereigns in the Eurozone (European Economic and Monetary Union), the financial strains caused by shifting demographics are being compounded by the current economic and financial troubles, which are both strangling growth and increasing the need for social safety net spending. This environment can result in tighter financing conditions amid private-sector deleveraging, plus cuts in public investment leading to a reduction in total investment and consequently the stock of capital. At the same time, the decline in investment activity will likely hurt total factor productivity (a measure of an economy’s technological innovation). Adding to these adverse trends, low employment and net emigration from several sovereigns implies a smaller contribution of labor to future economic growth, a continuing threat if unemployment becomes structurally high.As can be seen, Standard and Poor’s mention a number of other factors which contribute to what they call the current “strangling” of economic growth in countries like Spain (tighter financial conditions, private sector deleveraging, cutbacks in public sector infrastructure spending, net emigration).

They could also have cited the mere existence of the euro. It is evident that participation in the common currency has had the perfectly foreseeable effect on Spain of making it simple to get into trouble and a lot harder to get out of it. Borrowing was cheap and easy of access during the boom years, now lending to Spain’s banks has all but dried up, and what there is available remains burdensomely expensive.

Divergences in interest rates paid by businesses on bank loans across the Eurozone have recently reached record highs, despite ECB attempts to achieve the opposite result. While the spread between yields on Spanish 10-year bonds and their German equivalent has narrowed significantly the Goldman Sachs interest rate divergence indicator – a measure of cross-border variations in rates charged by Eurozone banks on a selection of business loans – has once more risen and reached 3.7 percentage points in January. This means that companies in southern Europe continue to pay significantly higher interest rates than their northern rivals, leading to the conclusion that while ECB measures may well have been effective in avoiding short term Eurozone break-up, they have still failed to address the problem posed by such inhibitive credit conditions along the southern periphery.

The lessons learned from inaction

So not only does Spain have uncompetitive productivity levels, and a damaged brand image, it also has a high cost of new capital making investment in the country’s economy both unattractive and prohibitively expensive. With unemployment at over 26 percent, non-performing bank loans remain on their upward path, meaning that more companies are facing potential insolvency. The recent bankruptcy of food multi-national Pescanova has renewed rumours in financial circles that the Bank of Spain is preparing another round of provisioning increases – this time for loans to large corporates and small and medium companies – is an indication of how severely the crisis is now hitting the entire business sector. The Spanish problem is now no longer simply one of a construction collapse, since the ensuing impact on overall economic activity has now spread right across the board. A stitch in time saves nine, as the saying goes, but in the Spanish case there was no stitch (since according to policymakers there was no deep-seated issue to address) and the garment simply unravelled. Lesson – it is a lot easier to make things worse by inaction than it is to make them better using the same approach.

But backtracking a bit, the euro makes correcting Spain’s present situation difficult due to the absence of a national central bank able to conduct a full range of monetary policy operations, a limited access to fiscal policy and the fact the country has no currency of its own to devalue. But that does not mean, as Wolfgang Munchau recently suggested, that it is becoming more and more rational to think about euro exit as the cost-of-leaving threshold gets lower and lower. Countries may well one day leave the euro, but if they do it will be because the cost of trying to hold it together has driven them all but mad, not because they have made some back-of-the-envelope calculation showing that the benefits outweigh the costs. Leaving the euro would be a huge leap into the unknown, leaving one side of the calculation sheet simply beyond our ken. As I argued in a post for the CNN blog, the currency bares an uncanny resemblance to Dr Strangelove’s doomsday machine, designed so that one day it would almost inevitably blow up the global financial system, but constructed so that any attempt to dismantle it would also produce the same outcome.

Yet, despite the risks, as Gideon Rachman puts it in the Financial Times, in today’s Spain people are slowly but surely losing their faith in both national and EU institutions, and are slowly being driven towards ever more radical “solutions” which far from being rational bear a pretty strong resemblance to the exact opposite:

The “European dream” that Spaniards embraced promised a middle-class lifestyle for most people. But with little prospect of secure jobs for the young and a threat to the future of the welfare state, the fear now is that the Spain of the future will look more like Argentina than Germany. An Argentine future would involve the constant fear of financial crises – and a widening gap between the social classes, as many continue to enjoy a first-world lifestyle, while a growing underclass becomes detached from prosperity. Above all, Argentine public life is characterised by deep cynicism about national institutions and leaders.Leaving the euro would be an incredibly costly decision for Spain, and becoming yet another Argentina would surely be no panacea, but that doesn’’t mean it won’t happen.

Following in the Footsteps of Japan?

Meanwhile Mariano Rajoy struggles on. Since it is quite obvious that the current policy mix isn’t working, and with one eye on the growing number of “platforms” out there desperately seeking his scalp (those affected by the mortgage crisis, those affected by the preference share haircut) he is desperately thrashing around for a fig leaf policy to stop the nightmare. Last week he found one – in Japan. “I think in Europe we must all ask ourselves whether the ECB should have the same powers as other central banks around the world,” he told a press conference. In particular he seemed to be thinking about what he described as the “very important” shift in monetary stance that had just been undertaken by the Bank of Japan. Now here is not the place to go into the background to the Japan crisis (see my arguments here if you are really interested), but one thing I am sure about is that neither Rajoy nor his main policy advisers have any real idea about what lies behind Japan’s long lingering deflation problem. What he does know is that Japan is able to run a 10-percent fiscal deficit and a 235-percent government debt-to-GDP level with what Nobel economist Paul Krugman calls “no evident ill-effects”. Sounds good to Rajoy. Will it work in the long run? “No idea”, could be his response. In the long run, as is well known, we are all dead, and “anyway I won’t be in the Moncloa” might easily be his reply.

In fact, as billionaire investor George Soros recently warned, systematically debasing a currency (ie not just conducting a one-off devaluation) is an extraordinarily dangerous move. The Bank of Japan has, in Krugman’s words, committed itself “to credibly promise to be irresponsible”. What this “irresponsibility” means is devaluing the currency sufficiently every year to generate sufficient price rises to comply with the central bank’s recently announced 2 percent annual inflation target. This is one promise it will be hard for the bank to keep since Japan’s deflation is being caused not by a poor adjustment in the economic system by structural demand deficiencies produced by the country’s ageing and shrinking population.

The best case scenario would be that the country’s policy makers realize in time that the experiment won’t work, and come to recognize that they have to learn to live with deflation – in which case the only big headache they will have will be what to do with all that debt (you know, the debt that many thought presented no evident problem). Far worse would be success, since if the Bank of Japan succeed in changing expectations (not in the why, but in the how) and lead people to believe that the currency will be debased every year ad infinitum (even assuming the rest of the G20 could ever agree to this), just to guarantee that 2-percent inflation, then they may well end up forgetting their supposedly innate “home bias” and start converting as many yen as they can get their hands on into dollars or some other convenient monetary unit, in the process creating a run on the currency which will make what happened in Argentina look like child’s play.

Such details are doubtless lost on Mr Rajoy and his advisers, which is just my point. The current crisis – which is arguably no longer a crisis but rather a way of life – has all now gotten so complex that the issues involved are almost certainly, and in principle, “beyond their ken.” Spain’s economy will continue to march boldly forward towards what now seems almost guaranteed to be long term decline, while from within the captain’s tower, far from an acceptance that what is happening really is happening, we will continue to hear yet one more crazy and implausible story after another telling us “if only this”, or “if only that” even as representatives of the Plataforma de afectados por las hipotecas (or equivalents) start to assemble outside the local version of the winter palace looking for their hides.

Postscript

I have recently established a dedicated Facebook page to campaign for the EU to take the issue of the Euro Area accelerating population imbalances more seriously, in particular by insisting member states measure movements of their own national populations more adequately and also by having Eurostat incorporate population migrations as an indicator in the Macroeconomic Imbalance Procedure Scoreboard in just the same way current account balances are. If you agree with me that this is a significant problem that needs to be given more importance then please take the time to click "like" on the page. I realize it is a tiny initiative in the face of what could become a huge problem, but sometimes great things from little seeds to grow.

This is a revised version of an article which originally appeared on the Iberosphere website.

No comments:

Post a Comment